My SHOUT-y friend Alison Inman asked an interesting question on Twitter last week. “Optimum size for a HA? How big is too big? How small is too small?”

It received dozens of responses, of which more below. But it reminded me of an article I wrote 21 years ago for Housing Today (now defunct) entitled Dawn of the Monster Age, describing the rapid growth of housing associations. It’s not available online but I’ve posted a copy of it here.

In the article, I asked a few questions and made a few statements. Some examples:

“How long before we see the first RSL with 50,000 units?”

“In the mad rush for growth, the future for small and medium-sized housing associations seems bleak”

“Big is beautiful seems to be the new orthodoxy”

“My experience of large landlords is that they tend to be remote from their customers, poor at internal communications and struggle to provide a good service”

“At a time when the break-up of large monolithic local authority portfolios is being actively pursued, it seems to me strange that that we are promoting the growth of even larger RSL landlords, which have both a fuzzier geographical focus and poorer levels of governance and accountability than their local government counterparts.”

“Are we in danger of slaying one set of monsters in order to create another?”

I went on to compare and contrast the two very different associations I’d worked for: one large (Circle 33, since absorbed into one of the very largest providers); and one small (Hundred Houses – it still exists as an independent outfit).

My analysis of the data at that time was that big was not necessarily better.

Anyway, the responses to Alison’s question were very mixed. The consensus was that there was no consensus, although geography seemed important for some people. One said:

“It’s not size that matters, it’s spread. Being over-spread leads to remoteness of decision-making, poor service, inefficiency and no role in social and economic regeneration. There’s no upside to spread. There are some benefits to size, if it’s a lot of homes in one area”

Others said:

“…it depends on geography, origins, history, situation and circumstances… I am not really sure there is one size fits all”

“If you need more than one office to be logistically viable and connected to your residents – you’re too big. If you employ <20 people you’re (probably) too small.”

To which one smart aleck replied: “Why does a housing association need an office?”

“20,000 optimum in my opinion within a 1-hour travel distance of main property management hub.”

“10,000 max in a given geographical area.”

There seemed to be a common view that the largest associations had lost their way:

“I used to work for a very large HA. I left when it lost its soul and became far too corporate and more interested in the corporate brand than the customers. In a smaller organisation it’s easier to find solutions for customers and think outside the box/try something different.”

“I think any HA that is more than 50,000 is too big and I think too small is anything below 500”

“Having observed the evolution of Housing Associations since about 1976 I’d say about 6k. 100k is obscenely, inefficiently large. Lumbering beasts”

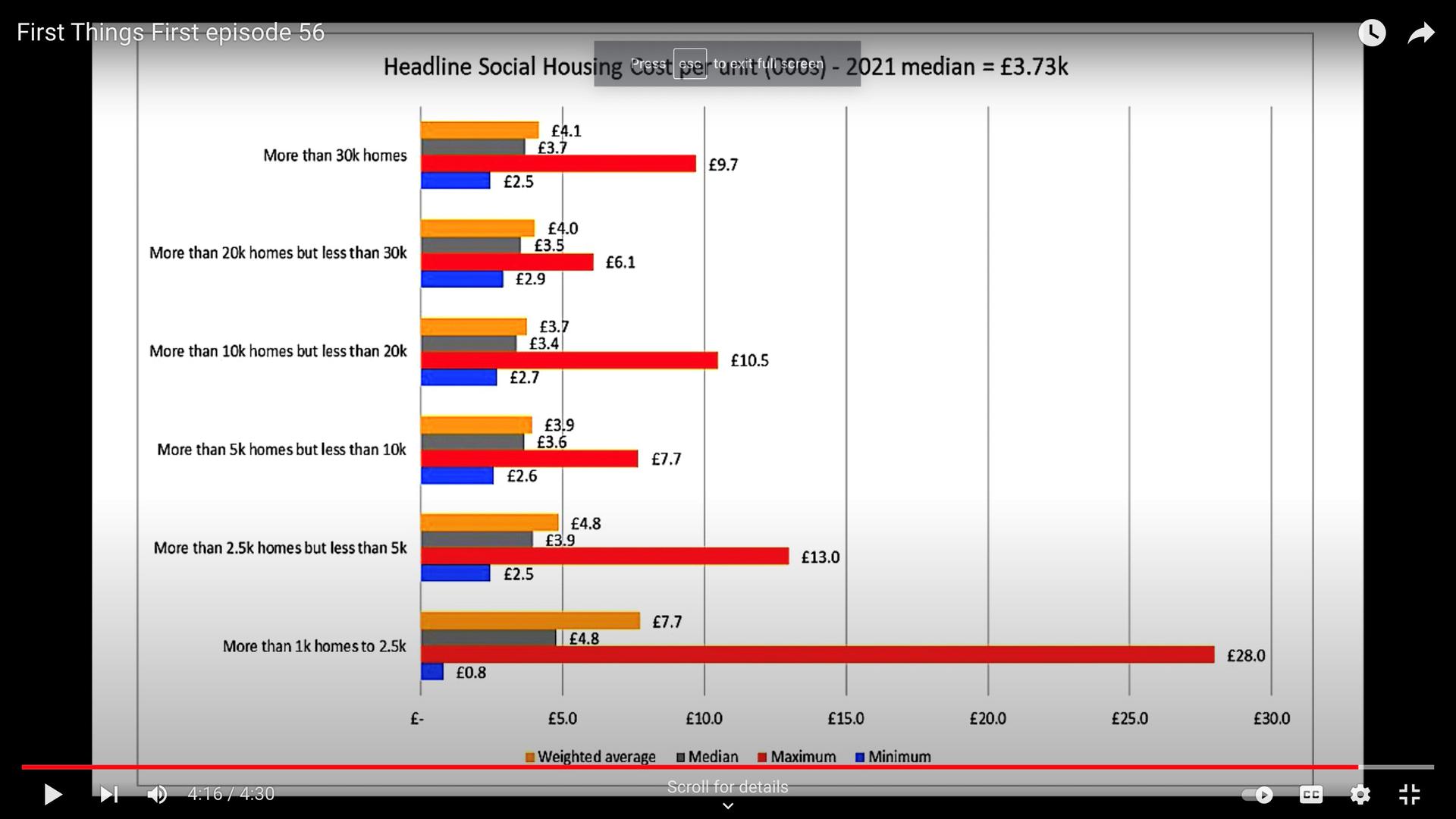

The analysis supplied by Ian Parker at HQN quoted by Alistair in his latest YouTube presentation is that there’s no clear link between size and costs above 2,500 homes. Associations below 2,500 homes have much higher median costs of £4,800 per annum but the lowest median cost of £3,400 per annum is in the 10 to 20,000-home cohort, whereas above 30,000 homes this rises to a median cost of £3,700 per home.

There are significant outliers in each cohort but this analysis doesn’t tell us anything about overall resident satisfaction – how “good” an association actually is – so, the proposed tenant satisfaction data proposed by the regulator might help us to join up the dots between size, costs and satisfaction.

But compare, for a moment, our sector to the wider corporate world. McDonald’s and Amazon are found all over the world. Whether you eat a Big Mac in Bristol or Brisbane, the quality and customer service will be of the same standard. Amazon parcels are delivered just as efficiently whether you’re in Camden or Canberra. Neither of these firms think for a moment that an optimum size is desirable. Their aim is global domination, and customers seem to like their products and service.

In my work for some HQN it’s notable how some very large providers appear in the tables for complaints and regulatory interventions again and again, whereas similar sized rivals/peers rarely appear. It seems to me that the issue isn’t so much about size as about leadership, culture and a relentless drive for improvement.

So, in answer to Alison’s question perhaps the answer should be as follows:

“What’s the optimum size for an association that’s badly led, has a poor culture and unhappy tenants and isn’t bothered about improving? Answer: zero homes.”

“What’s the optimum size for an association that’s well led, has a great culture and happy tenants and a relentless drive for improvement. Answer: no optimum, no limit.”

Anyway, no doubt this debate will go on and on and if I’m still around 21 years from now perhaps I’ll be writing another article with a different perspective.

But thanks to Alison for posing the question.

{kind=link}

{kind=link}